Time to sell student rental REIT Unite Group (UTG)?

UK’s higher education sector is a multi-billion industry.

Many students value the prestige of a quality UK degree. Graduating from ‘OxBridge’- short for Oxford and Cambridge – carries a distinct premium in the job market.

In the years before the pandemic, the numbers of students – international and domestic – arriving on UK campuses soared.

Property companies that provided student accommodation captured this growth. ‘Build and they will come’ was the one and only business model. Rental income rose; as did the stock prices of these student accommodation REITs.

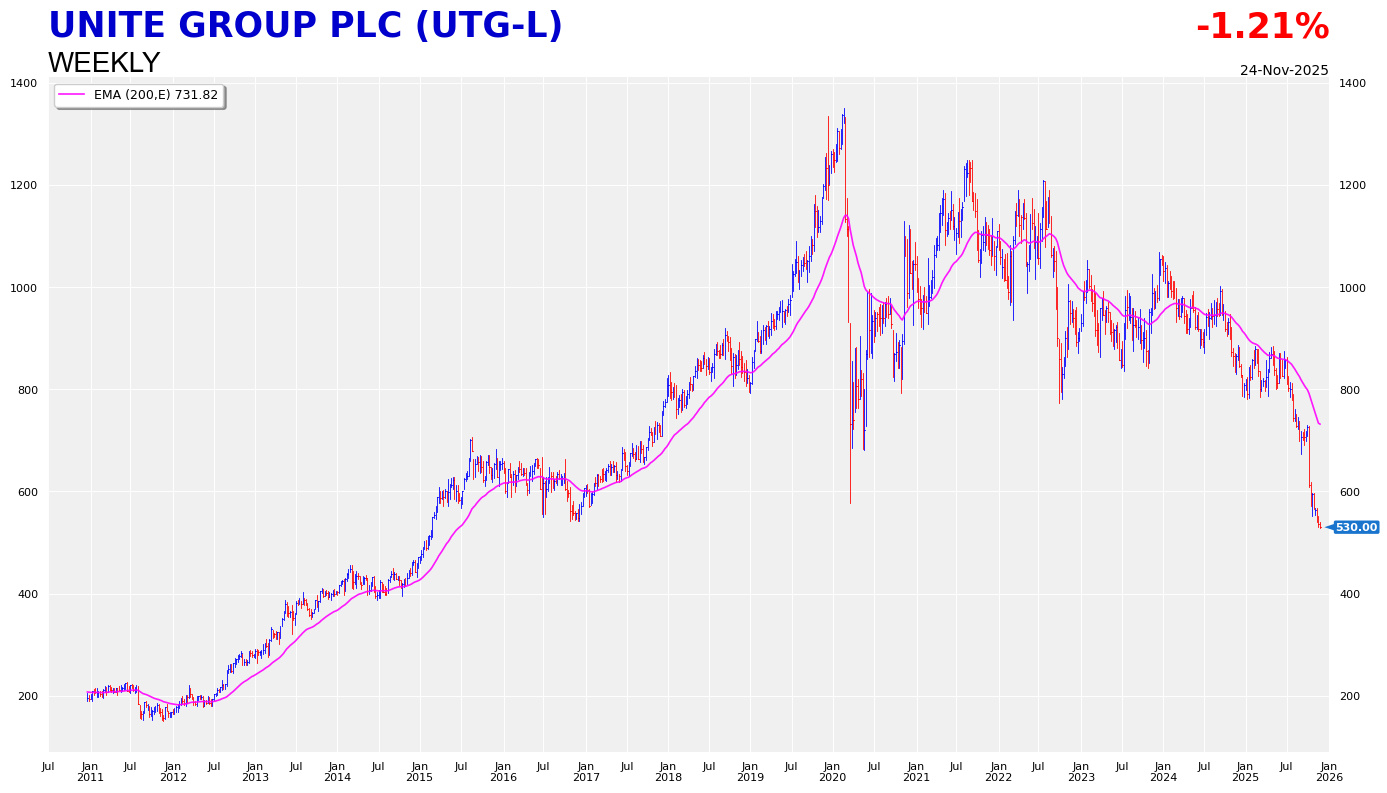

Unite Group plc (UTG), the largest purposed-built student accommodation PBSA, saw its share price gain 7x in 8 years (2012-2020).

But the pandemic caused a structural shift in the global education market.

Yes, students kept registering on UK universities. But growth inevitably slowed.

Moreover, UK university fees for international students kept climbing; while other costs also increased sharply in the post pandemic years.

Recently, the Chancellor proposed an additional 6 percent levy on international fees. This will further increase the cost of UK degrees. [1]

No wonder investors are becoming pessimistic on the sector.

Unite Group saw its share price halved in 18 months to sit at 10-year lows.

As its weekly chart shows, the downtrend here is strong and persistent. Prices are trading steadily below the long-term moving average. Support may emerge at 500p, but that’s not a certainty.

The plus point of buying this £2.6 billion REIT now is its high yield (around 7 percent). But given UTG’s prolonged share price decline, this yield may fatten considerably in the months to come.

A more pessimistic scenario is that UTG’s share price may even halve again from here.

In sum, Unite is facing structural headwinds that may not lessen over the medium term. If long, rallies may be used to lighten positions for potentially better entries.